Ryan George is the Chief Marketing Officer at Docupace. He is responsible for the company’s brand awareness, early-stage sales pipeline, content strategies, customer and industry insights, internal and external communications, design, and events. George actively engages in leadership roles in both the financial services and marketing communications communities. He a member of the Forbes Communications Council, an invitation-only, fee-based organization of senior-level communications and public relations executives, the CMO Council and the CMO Club.

One of the easiest ways for wealth management firms to streamline their backend processes, improve relationships with investors, and meet compliance requirements is to implement e-delivery across their systems and processes.

It’s hardly a secret that going paperless is the way of the future. RIAs and investors alike have come to expect paperless delivery (or a paperless option, at the very least) wherever they do business. Indeed, only 8% of investors want paper copies of their investments sent through the mail.

In this article, we’ll break down the benefits of e-delivery including time, money, and compliance, and highlight how Docupace’s TRACKR™ can help wealth management firms adopt e-delivery even faster.

The Business Case for Adopting E-Delivery

The best investor/advisor relationships hinge on good communication. Similarly, the best wealth management/regulatory relationships also depend on good communication. Without clear expectations, quick feedback and efficient communication, wealth management firms are less likely to have great relationships with their investors and stay compliant.

That’s where e-delivery comes in. Electronic processes improve communication capabilities by allowing advisors to spend more time with clients than on paperwork. Not only that, but clients are already comfortable with e-delivery.

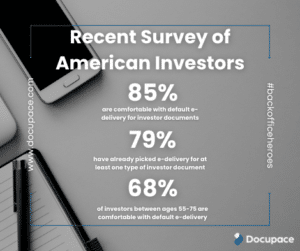

In a recent survey of American investors:

- 85% are comfortable with default e-delivery for investor documents.

- 79% have already picked e-delivery for at least one type of investor document.

- 68% of investors between ages 55-75 are comfortable with default e-delivery.

If there was any lingering doubt, wealth management firms should consider the savings they can experience through e-delivery. Going paperless can reduce disclosure processes by 65%, allowing advisors to spend more time with clients. Additionally, firms can save $7.75 per electronic disclosure by cutting out the mailman.

The business case for adopting e-delivery is compelling. But staying compliant can offer even more savings.

How E-Delivery Cuts Down Compliance Costs

Compliance has become even more complicated in the last few years. Between Reg BI (Form CRS), Form ADV, and DOL Rules requirements, many wealth management firms have had to scramble to stay compliant. This inefficiency translates into real sunk costs.

Deloitte estimates that compliance costs companies at least 4% of revenues, with that number expected to jump to a staggering 10% for firms “unable to effect significant efficiency savings.” Indeed, nearly half of U.S. wealth management firms report that their systems and processes are under “severe strain” or need to be changed entirely in order to meet organizational objectives.

For companies facing compliance woes, e-delivery can turn things around. For example, Docupace’s TRACKR™ enables companies to:

- Automatically generate disclosures based on customizable parameters that ensure the content in each disclosure is up to date.

- Delivery disclosures electronically to investors instantly.

- Store relationship summaries securely according to 17a3- and 17a4 compliance requirements.

E-delivery can create an environment where compliance is simple from start to finish.

Benefits of Docupace TRACKR™

When it comes to e-delivery, Docupace has over 30 years of experience helping companies stay compliant. Our technology was built specifically for RIAs, their customers, and the internal “back office heroes” who can benefit most from e-delivery.

Our platform was designed for wealth management, so there are no features you don’t need or want. Built with compliance oversight tools, we can help you reduce costs, store documents securely in the cloud, and provide a truly digital experience that clients will love.

Here are just a few of the many ways that firms benefit from our innovative TRACKR platform:

- Use automated workflows and CRM integrations to digitize Reg BI (Form CRS), Form ADV, and DOL Rules disclosures.

- Use a hyper-secure digital vault to store records in a FINRA/SEC-compliant way.

- Use on-demand audit trails and real-time reporting to stay compliant.

- Use time-stamped delivery of disclosures with our proprietary “digital first, analog second” client attestation process.

If you’re interested in unleashing the power of e-delivery with Docupace, explore our full platform or reach out to us here.

With compliance regulations shifting and fees increasing (the SEC reported a 7% increase in enforcement actions in 2021), it’s never been more important for wealth management firms to instill a culture of compliance.

Whether your firm is large enough to employ a dedicated chief compliance officer or only has a handful of employees, prioritizing compliance offers many benefits, including lower regulatory fees, fewer infractions, and a reputation for integrity.

What is a culture of compliance? It means making compliance a hallmark of your firm, not an afterthought. It means training all advisors and employees to understand the definition of compliance and its impact on their daily actions. And it means fostering an environment where employees aren’t tempted to cut regulatory corners, no matter how small or unintentional they may be.

Here are three ways to create a culture of compliance:

Keep Advisors Up to Date on Changing Regulations

A culture of compliance starts at the top with leaders who understand the importance of following regulations and providing ethical services. But that mindset isn’t effective if it isn’t disseminated to all advisors and employees through regular training.

Regulations are constantly changing, and it can be challenging for advisors and back office employees to keep up amid their other responsibilities. Regular employee training on regulatory updates, either through dedicated quarterly training or short updates at all-hands meetings, ensures everyone is up to date on compliance standards.

Talking about compliance and making it a filter for decisions in every function of your business integrates compliance into your firm’s daily activities and the minds of your employees.

A training needs assessment can help you identify your firm’s highest risk areas. Compliance is complex, with many potential topics for compliance training to cover. A wealth management firm for high-net-worth individuals will likely have different compliance challenges than an RIA firm focused on small businesses.

Understanding previous compliance concerns and the issues most at stake in your firm can guide training to focus on the most relevant areas.

Leverage Technology to Automate Compliance

Technology opens doors to new compliance issues but is also useful for scaling and automating compliance efforts. Even with comprehensive and regular training, mistakes can happen. Supporting compliance efforts with technology helps advisors follow through with their best intentions.

Investing in compliance-enabling technology also shows employees how much the firm values compliance. Firms can make maintaining compliance easier for everyone by providing advisors and employees the right tools.

Compliance technology, or regtech, enables employees to process and store firm and client data efficiently and correctly. With increased numbers of advisors and employees working remotely, it has become especially important to ensure everyone has access to the correct information and that it is stored and accessed properly.

Platforms like Docupace automate document storage and processes and integrate compliance protocols to automatically raise red flags and ensure all regulations are followed.

Create Clear Compliance Protocols

In a culture of compliance, employees not only know what it means to be compliant but also what to do when they see a breach in compliance.

Although one person may be in charge of compliance efforts, the firm should delegate reporting responsibility to everyone. Shared compliance accountability requires creating a clear reporting structure and providing ways for employees to comfortably report concerns.

Thomson Reuters put it this way: “In the wake of unprecedented regulatory reform and compliance overhauls, financial firm leadership must adjust its perspective and view individual employees as their most valuable resources in the detection of criminal behavior.”

One of the biggest compliance risks for firms isn’t employees overtly breaking the rules but instead becoming complacent. Overlooking seemingly minor issues can lead to major compliance oversights and a general lack of regulatory integrity. A safe environment where compliance is expected encourages employees to stay vigilant instead of becoming careless.

Many firms create compliance plans or processes but don’t share them with employees. The most effective processes involve all employees and are regularly re-evaluated and updated as regulations and firm needs change. Regular compliance audits and reassessments of your firm’s reporting plans will help you develop current, employee-supported compliance procedures.

All firms today need to create and foster a culture of compliance. By empowering employees with training, technology, and processes, compliance can become the foundation of your firm.

For brokers and wealth management firms, record keeping is more than just holding onto old forms. It demands a comprehensive system to maintain, store, and organize the required documents to stay in compliance.

Unfortunately, there are hundreds of ways record keeping can become a broker’s compliance downfall.

Here are four common record keeping pitfalls and how to avoid them.

1) Not Maintaining a Comprehensive Set of Records

Financial planning and broker dealer record keeping is more than saving copies of contracts, trades, and bank statements. SEC Rule 17a-4 specifies the manner and length of time that the records created and produced by broker-dealers, must be maintained, and produced promptly to SEC examiners. To comply with FINRA and the SEC, brokers and firms of all sizes must keep a comprehensive set of records, including employment applications, website copy, trade confirmations, and asset and liability ledgers. Failing to retain even one type of record can put a broker out of compliance and lead to serious fines and punishments. [1]

But keeping track of all those documents can be daunting. Because they must keep copies of nearly every type of document and correspondence, many brokers get overwhelmed and fail to stay in compliance across the board.

2) Using Disconnected Data Storage Tools

Keeping records isn’t just to check a compliance box but to have the correct documents accessible when needed. Under Books and Records, documents must be easily accessible for the first two years. But too often, brokers and firms use different systems for different types of recordkeeping. They may archive client emails within their email system, back signed contracts to the cloud, and keep paper copies of client intake forms or marketing materials.

Although these formats technically all keep the records in compliance, it can create a headache when the firm is audited and has to track down a wide variety of documents or if a client has an issue and the broker needs to locate the corresponding paperwork. When documents are stored in various formats on disconnected systems, finding even a simple email or signature takes up valuable time that could be put to better use serving clients or securing deals. Even worse, if a firm can’t find the correct document on its various systems, it could be held out of compliance even if it does have the right form but just can’t find it.

3) Not Holding On to Records Long Enough

Even brokers who hold onto the correct records often don’t keep the files for the right amount of time. According to the SEC’s Books and Records rule, brokers must keep the originals of all communication received and copies of all communication sent for at least three years — including bank statements, bills, and other business documents. The length of time records must be kept ranges from three years to 22, depending on the type of record.

Getting rid of documents too soon or not holding onto records for the required amount of time can lead to compliance issues.

4) Using an Outdated Record Keeping System

The record keeping rules brokers and firms must follow change regularly. But brokers who don’t stay up to date with changes risk following outdated practices and not being in compliance.

Effective Data and records management isn’t a one-time thing. As technology changes, the SEC and FINRA have updated what type of records need to be kept (such as adding the requirement to maintain social media posts) and updated requirements for electronic record keeping in SEC Rule 17a-4 (f). Staying in compliance requires staying up to date with the changes and regularly updating the firm’s data management system to ensure it is holding on to the proper records and following the current version of the rules.

The best way to solve these common mistakes is with an integrated data management system like Docupace. These systems automate data storage to ensure the correct forms are kept for the appropriate amount of time and in the proper format. And because integrated systems connect all the tools used within the firm, everything from bank statements to social media posts and client emails is kept in one cloud-based location that is easy to search. The answer to all your record keeping headaches is simple: Docupace’s integrated document management solution.

For more information about Docupace and a demo of how it can transform your firm’s recordkeeping, contact us.

[1] SEC.gov | SEC Charges 16 Wall Street Firms with Widespread Recordkeeping Failures

Managing retirement savings is one of the most crucial aspects of wealth management. After all, most investors have worked, quite literally, their entire lives to save for their post-retirement future.

To protect clients’ best interests when it comes to retirement savings and rollover recommendations provided by financial institutions, the U.S. Department of Labor (DOL) added a new compliance rule for finance professionals called the Prohibited Transaction Exemption 2020-02, Improving Investment Advice for Workers & Retirees (PTE-2020-02).

With the final compliance deadline of June 30, 2022 in our rearview, it’s time for wealth management firms to get in line. This blog will discuss what you need to know about PTE-2020-02, how to comply with the June deadline, and a few common mistakes to avoid.

What Is PTE-2020-02? A Timeline

The main goal of PTE-2020-02 is twofold: First, to protect investor’s best interests when it comes to rollover retirement savings. Second, to enable fiduciaries to receive compensation under the exemption by requiring them to prove (and document) that any rollover advice is in the customer’s best interest.

Despite PTE-2020-02 already largely being in effect (it was passed in December 2020), the DOL has given certain extensions in order for firms to become compliant. Here’s a quick refresher on the timeline for PTE-2020-02, including key deadlines that wealth management firms need to comply with.

A PTE-2020-02 Timeline

- December 18, 2020: PTE-2020-02 announced by DOL.

- February 16, 2021: PTE-2020-02 goes into effect.

- April 2021: The DOL releases a FAQ page about PTE 2020-02.

- December 20, 2021: DOL will not pursue claims prior to this date to provide transitional relief for fiduciaries working in good faith to comply with “Impartial Conduct Standards” in PTE-2020-02.

- October 25, 2021: In Field Assistance Bulletin 2021-02, the DOL extends non-enforcement policies through January 31, 2022.

- February 1, 2022: Deadline for fiduciaries to comply with all but documentation and disclosure portion of PTE-2020-02

- June 30, 2022: Final deadline for fiduciaries to comply with all requirements of PTE-2020-02, including the proper documentation and disclosure procedures outlined.

As you can see, all of the enforcement and implementation deadlines have long passed. In the next section we’ll discuss why this is, and what type of documentation you’ll need to comply.

Three Requirements for Disclosure & Documentation Under PTE-2020-02

There are three main disclosure requirements for investment professionals under PTE-2020-02, as explained in the DOL’s FAQ page:

- An acknowledgement of the firm’s fiduciary status in writing.

- A description of the services provided, expected fees, and any material conflicts of interest.

- Documentation of the reasons why a rollover recommendation is in the investor’s best interest, and that document being provided to the retirement investor.

While the first two disclosure requirements are more or less simple to comply with in a single document, the final requirement brings something entirely new to the table.

What should be included in a rollover recommendation disclosure for PTE-2020-02?

In the FAQ, the DOL expounds that the relevant factors firms need to consider in a rollover recommendation disclosure include but are not limited to:

- Fees and expenses associated with the rollover plan and an IRA

- Viable alternatives to a rollover, including leaving money in the investor’s employer plan

- How much employers pay for the plan’s administrative expenses

- What services and investments are available to the investor under the plan and IRA

In summary, wealth management firms must provide a full analysis of why a rollover recommendation is prudent that considers these factors and more. Streamlining and creating an entirely new compliant framework for a rollover analysis isn’t easy and is largely why the deadline for documentation and disclosure was extended until the end of June 2022.

For more tips on streamlining your documentation procedures, check out the Docupace blog here.

Avoid These 5 Mistakes to Comply With PTE-2020-02

Staying compliant with PTE-2020-02 is easier when you know some of the key mistakes to avoid. Here are five common mistakes firms make when it comes to PTE, and how to avoid them.

- Watch out for implied recommendations, and don’t try to get around the rule with creative wording in your disclosures.

- Remember that rollovers are defined broadly — it also includes IRA-to-IRA transfers, a qualified plan to an IRA, a plan to a plan, an IRA to a plan, or any change of account type from commission-based to fee-based for a plan or an IRA.

- “Plan” and “IRA” are defined broadly, plan accordingly.

- Make sure your fiduciary acknowledgement isn’t deficient — it should comply with both the Code and ERISA.

- Make sure to assess the reasonableness of compensation in your documentation. The DOL uses a market-based standard, so having benchmarking services to help might be prudent to comply with this requirement.

In short, to successfully comply with PTE-2020-02, wealth management firms need to ensure their documentation management systems are ready. Specifically, are there workflows, automated processes, and organizational protocols to ensure firms stay compliant with the new requirements? If not, you might consider a digital solution like Docupace to bridge the gap.

At Docupace, our cloud-based Compliance TRACKR™ helps advisory firms simplify and digitize client disclosure requirements. This solution is purpose-built to keep you on the right side of PTE-2020-02 and meet all the regulatory requirements. TRACKR sits on top ofour world-class documentation management software and helps compliance teams stay organized and efficient. With over 20 years in the industry, we’re a leader in helping wealth management firms stay compliant in an ever-changing landscape. Reach out to learn more here.

With several big changes and complex new rules, regulatory compliance is a going concern for wealth advisory firms of all sizes. Keeping up with the number of regulations firms and advisors must follow is burdensome, with regard to both time and money, but the even larger cost of noncompliance has been played out by Wealth Management firms and seen in the headlines over the last number of years.

It’s likely the cost of staying compliant for most firms, will help firms avoid paying the price for noncompliance. However, the cost of noncompliance is more than just regulatory penalties which seriously cripple a firm, it also causes brand damage and many times forces employees to spend time on tasks that they do not normally spend their valuable time doing.

Here’s everything you need to know about the true cost of noncompliance.

Fines and Penalties Levied by Regulators for Infractions

The most obvious cost of noncompliance are the fines and penalties seen in trade publications. In fiscal year 2021, the SEC assessed more than $3.9 billion in fines.

The fines and penalties vary according to the nature and severity of the compliance issue. Some instances bring a $5,000 fine. Others garner a temporary suspension as a FINRA member. And, of course, compliance issues can lead to multi-million-dollar fines against advisors and the firm itself. One of the most notable recent instances is FINRA’s action against Robinhood, which was ordered to pay nearly $70 million for supervisory failures and noncompliance.

Lost Time, Reputational Damage and Resource Drain

Noncompliance leads to greater costs than just paying penalties. Seemingly tangential costs also significantly impact a firm, especially in today’s competitive market. Damage to a firm’s brand or reputation, such as bad press, a loss of client trust, or a decline in employee morale, is costly. One study found that although the average penalty is $2 million, noncompliance leads to an average revenue loss of $4 million and $3.7 million in lost productivity, meaning that the regulatory fine itself is just the beginning.

In the post-pandemic world, trust is more important to consumers than ever, and they’re willing to change providers if they feel that trust is at risk. A survey by Deloitte found that 30% of a company’s annual revenues are at risk of consumer backlash for regulatory noncompliance — a staggering portion of the bottom line is contingent on reputation and it can come undone quickly when not staying in compliance.

Additionally, a lack of compliance can open the door to legal issues and additional fines or penalties. By putting clients’ information at risk and not staying in compliance, firms face the chance of legal action, which can start a lengthy and expensive process that eats up valuable resources.

Finally, there’s the opportunity cost of noncompliance. By spending time rounding up documents and working through the red tape of compliance issues and penalties, employees and advisors are spending less time building the firm and growing client relationships. A firm’s time and resources aren’t infinite, and any distraction by a noncompliance issue takes away from opportunities to grow and improve.

Cost to Comply < Risk to Not

Investing in a robust compliance system is just that: an investment. But it is a necessary cost of doing business that yields significant returns. Although compliance often comes with a cost (larger firms spend an average of $10,000 per employee on compliance efforts), it is a fraction of the cost of noncompliance. In general, the cost of noncompliance is three times greater than the cost of compliance. Some firms avoid systemizing their compliance efforts and fail to dedicate a portion of their budget to compliance technology and compliance programs because they don’t want to pull resources away from the bottom line. They do so at their own risk.

However, the positive impacts of staying in compliance, include a strong reputation, client trust, and increased productivity. These positives are proven to far outweigh the costs of being caught in noncompliance. An investment compliance technology and compliance programs is an investment in your firm’s growth and potential. Instead of paying more money later as damage control to right a sinking ship, you’re proactively investing in keeping your business in line with regulations.

Noncompliance is costly in its direct penalties and hidden costs that have a long-term impact on a firm. Investing in proactive compliance measures is the way to go to avoid the cost and headache of being caught in the dark web of noncompliance.

In the wealth management and financial advisory space, nearly everything you do is subject to regulation. Marketing/advertising must be pre-approved, emails are stored, text messages are captured and more. When it comes to a firm’s recordkeeping processes and efforts, very little is not scrutinized.

While recordkeeping may sound simple, compliance encompasses much more than just the records themselves – what you store, how you store it, where you store and how long you keep it are all have guidelines that must be followed.

Whether you are a financial advisor, back office professional or serve other roles within the industry, understanding these important regulations and requirements is crucial to staying within compliance.

Want (or need) to learn more? Here’s a simple guide to the basics of books and records and how it applies to wealth management firms.

What are the SEC’s Books and Record Rules?

Officially known as Rules 17a-3 and 17a-4 under the Securities Exchange Act of 1934, the books and records rule defines what records broker-dealers must retain and how long those records and other important business documents must remain on file.

Because books and records covers such a wide variety of documents, ranging from employment applications, client recommendations to canceled checks and email correspondence, it’s considered one of the most fundamental compliance rules.

The main goal is to set a universal standard and create consistency among wealth management providers. This uniformity assists the SEC, FINRA and even state securities regulators in ensuring all firms are in compliance.

What Types of Firms do Books and Records Requirements Apply?

All registered broker-dealers must follow the SEC’s books and records rule. The SEC defines a broker as “any person engaged in the business of effecting transactions in securities for the account of others.” Essentially, if you’re buying or trading securities, you must register with the SEC and follow the recordkeeping rules.

Failure to comply with books and records can lead to severe fines, both for the firm and the individual broker, as well as other punishments. Notably, JP Morgan was fined $125 million by the SEC and $75 million to the Commodity Futures Trading Commission (CFTC) in 2021 for failure to comply with recordkeeping rules.

The SEC, FINRA and other state and local regulatory groups take record keeping seriously. By following the SEC’s rules, firms and brokers will also be in compliance with other organizations.

What Are the Most Important Elements of Books and Records Rules?

The complete books and records rule is lengthy, but here the key components of the rule fall into three categories:

- What Activities Must Broker-Dealers Record? Broker-dealers must track the books, accounts, records, correspondence, and documents used to transact and run their businesses. These include asset and liability ledgers, securities records, trade confirmations, account ledgers, order tickets, employment applications, website and marketing material copy, and more. The records must be complete and accurate, meaning they can’t be duplicated or altered in any way.

- How Long Must Records Be Kept? Retention requirements depend on the type of record, ranging from three years to 22 years. Most record types must be kept for three or six years. The books and records rule states that brokers must retain originals of all communication received and copies of all communication sent for at least three years. Bills, bank statements, business agreements, and other documents also fall into the three-year category. For the first two years, those records need to be easily accessible.

- What Format Should Records be Stored? Firms may store their records in paper form, electronically or on micrographic media like microfilm. Electronic records have specific requirements detailed in SEA Rule 17a-4 (f), most notably that they must be stored in a system that meets specific requirements.

The Digital Organizer from Docupace

Docupace provides a secure, digital and compliant solution for wealth management firms to centralize all of their client records.

- Automatically organize and store all documents in a secure digital vault

- Comply with rules 17a-3 and 17a-4

- Leverage true cloud-based WORM storage

- Assign roles and permissions to manage who has access to which records

- Track user actions to identify suspicious activity

Click here to watch a quick overview of the Digital Organizer.

Of all the compliance issues firms and brokers face, books and records is perhaps the most important and the most scrutinized. Although it’s helpful to understand the basics, reading the entire regulation can help ensure you and your firm stay in compliance.

The financial world has a plethora of acronyms that can sometimes seem overwhelming. One in particular to pay attention to is NIGO. NIGO stands for “Not In Good Order,” a reference to financial, insurance, and other paper documents submitted by customers and investors before initiating transactions. As the name implies, these documents are typically lacking in important information — or, in some cases, have inaccuracies — that need to be corrected before processing.

On average, a surprisingly high amount of documents submitted to back offices can fall into the NIGO category and can significantly slow down processing times. Many documents contain sections that only pertain to certain investments, account types or registrations and having the wrong fields filled out can cause major confusion and errors.

Wealth management and investment firms need to understand how to quickly and efficiently mitigate the submission of NIGO documents. This post examines the major problems caused by NIGO paperwork and strategies for combating its most negative effects.

Mitigate Errors with Better Document Preparation

At the bare minimum, NIGO documents require back-office staff to fix errors. Setting out on what can feel like a “wild goose chase” of information-hunting from investors and customers can be tedious and time consuming. There’s no doubt that NIGO documents cost companies in fees and employee time significantly more than those submitted correctly in the first place. Sometimes, really problematic NIGO forms can require multiple rounds of revision and fact-checking for firm staff.

Even the simplest mistakes can cost businesses in creating NIGO documents. Key punch errors, typos, and putting information in the wrong form fields can create significant backlogs and result in incorrect recommendations. These errors have the potential to multiply when workforces are largely remote or hybrid. PWC found that 69% of financial services companies reported that a majority of their employees would continue to work from home at least once a week. A scattered employee base means that automation, accuracy, and consistency are even more important in a post-pandemic business world.

Administrative costs related to reprocessing can also be high in manpower hours. Instead of completing other tasks, a good chunk of staff members’ time can be spent reprocessing NIGO documents. Not only is this work redundant, it can also potentially lead to further inaccuracies as employees are increasingly unable to pay attention to other important logistical details of their jobs.

These issues cause frustration on a one-off basis, but when NIGO documents are coming in consistently to reviewers, it can have a substantial effect on a firm’s bottom line. Finding innovative tech solutions to these problems can help shore up firms against future NIGO impacts.

Recognizing How NIGO Impacts the Customer Experience

High NIGO rates also have repercussions on the customer experience. Although the cost of updating NIGO documents is high from an administrative standpoint, it’s even more costly to not invest in error correction.

Incorrect documents lead to bad recommendations and financial decisions, which ultimately risks the trust between investors and clients. This negative experience can cost a firm otherwise loyal clientele and result in high investor abandonment rates.

Having a trustworthy advisor is the single most important factor for customers considering long-term relationships with firms. Breaking that trust – or failing to cultivate it in the first place – can push customers to competitors and result in negative word-of-mouth. Although the retail world is very different from that of finance, the same principles apply for both shopping behavior and the strategic selection of investors. Thirty-two percent of consumers reported that one bad experience is all it takes to abandon a company for good, even if previous brand interactions had been positive. When it comes to personal finances, it’s a good bet to think that negative experiences – some of which are undoubtedly caused by NIGO errors – can cost firms customers.

Strategies to Prevent NIGOs

High NIGO rates in particular have the potential to truly hurt customer relationships. The good news is that several strategies exist for mitigating NIGO documents from being submitted in the first place.

One way to cut down on NIGO documents is to eliminate physical paper trails whenever possible. It’s far easier to misplace hard copies or have missing pages when documents aren’t stored on a digital cloud or software platform. Across the financial industry, issues with paper applications accounted for 60% of firms’ total NIGO rates. Moving towards an online storage solution can help cut down on the risk of losing documents and also provide a more secure experience for customers.

Similarly, transitioning to electronic signatures instead of manual ones can help expedite processing and make sure that customers are signing in all the right places. Many digital e-signature applications don’t allow users to submit documentation until all required fields have been filled in. It also allows customers to easily store and print their documents electronically.

Ultimately, the adoption and implementation of digital solutions can help eliminate or reduce errors by automatically populating documents, correcting typos, and performing security verification checks. Recent research from the Harvard Business Review reports a 65% reduction in costs and 90% reduction in turnaround times for firms with strong digital processes. Perhaps most importantly, digital solutions around the proper handling of documentation can increase trust between advisors and clients. This goal more than anything else can help firms cultivate long-standing professional relationships with customers that result in better investment advice (and increased profitability) for the long-term.

Interested in learning more about how digital operations technology can help your firm? Contact Docupace today for a consultation and get customized tips on how to process and digitize data, increase efficiency, and become more profitable.

It’s no surprise that compliance is a must for RIAs and wealth management firms.

Staying in compliance streamlines operations and helps avoid costly and time-consuming audits and fines. But it also can help build your business in another way: by helping bring in new clients.

In the competitive world of financial planning, compliance can give you an edge over the competition and set your firm on the path to growth in three key areas.

Competitive Advantage of a Strong Reputation

Most clients realize the risk inherent to financial planning and wealth management, but they also want to minimize that risk with an advisor they can trust. A strong reputation is worth its weight in gold and can be a powerful way to attract new clients. Staying in compliance builds your reputation and can bring in new clients because they know you will take care of their accounts and personal information.

When given a choice between an advisor who is known for staying in compliance and one who isn’t, new clients will almost always choose the advisor they can trust. That’s a huge competitive advantage that can set you apart from other firms.

Staying in compliance and building trust does more than just bring in new clients — it encourages existing clients to refer your services to family and friends. Studies found that 94% of investors are likely to make a referral when they “highly trust” their advisor. Referrals are one of the best ways to grow your business, so the impact of a trusted reputation can’t be understated.

Staying in Compliance Provides More Time to Serve Clients

Compliance issues can be draining to a firm and advisor, both financially and time-wise. Even minor compliance issues can cost firms thousands of dollars in fines, plus the time to sort through paperwork, track down documents, and work through the mountain of paperwork brought by incompliance. Larger issues can bring even heavier fines and take longer to resolve — and the cost of compliance is only increasing.

During that time of recovering from compliance issues, firms of all sizes miss out on providing excellent service to clients and building relationships with prospects. Even if non-RIA staff respond to compliance issues, it still becomes a drain on the entire firm’s resources. It’s hard to showcase your firm’s abilities and make sales when you’re tangled in compliance red tape.

On the flip side, having an established and automated system for your files that ensures everything is in compliance provides you peace of mind and gives you more time to build your business by reaching out to clients and building relationships. Instead of being in the weeds of compliance issues, you can look at a big-picture strategy to move your firm forward and gain new business.

Compliance Helps Build Out Desirable Digital Tools

Financial clients increasingly demand digital solutions to track and access their accounts and connect with advisors. Firms that provide strong digital solutions have a considerable advantage over paper-based firms as they demonstrate their forward-focused mindset and leverage the speed and efficiency of using digital tools.

Managing compliance significantly increases your digital tools because digital file storage and organization are already in place. When you use tools like Docupace to automate data storage and streamline back-office tasks with compliance in mind, you also build digital tools for other purposes.

An integrated digital solution does more than just increase compliance — it creates strong digital services across the entire firm, both for clients and employees. Robust internal digital solutions relieve bottlenecks for advisors and allow for faster and more transparent service while ensuring that accounts and documents are in compliance. Robust external digital solutions keep clients in tune with their accounts and empower them to reach their financial goals.

The benefits of compliance go beyond just avoiding costly fines. By creating a digital-first compliance system, you can bring in new business and grow your firm. In today’s competitive market, prioritizing compliance is required to attract new clients.

The topic of trade surveillance can frequently elicit groans of frustration from RIAs and wealth management firms. The task of screening for and addressing potential market manipulations and unsuitable trades seems overwhelming in the face of millions of data points and outdated compliance processes. Luckily, there are ways to navigate an update to your trade surveillance system that will save your firm time and energy. Here are three tips to keep in mind when optimizing your trade surveillance systems.

Understanding Why Trade Surveillance is Challenging

Before evaluating your current trade surveillance process, take time to understand the overarching problems that firms have faced when attempting to monitor trading behavior. Historically, automated trade monitoring has translated into vast reports of false-positive cases. These “false alarms” can result in relationship managers (RMs) spending up to 60% to 70% of their work time on non-revenue generating activities. Typical trade surveillance identifies relevant data sources, generates alerts of potentially non-compliant activity, and completes time-intensive reconstructions of potential abuse scenarios. Then, if abnormalities are discovered, firms must take steps to remediate the issue and document the results.

Even worse, the effort put into adequately investigating all these false positive alerts resulted in a system that was “no longer managing risk in any real sense.” Not only were RMs essentially wasting their time, but real threats — initiated by traders clever enough to work around existing regulatory measures — went undetected.

Recently, the regulators have enacted increased regulation regarding trade surveillance, which means that wealth managers must take additional measures on the individual firm level to ensure compliance. As recently as December 2021, the SEC proposed new rules that would update compliance and security requirements for traders. In addition, legacy IT and surveillance systems have increasingly become defunct as more legislation requires data-intensive and consistent monitoring of risk signals. As a result, firms need flexible and automated solutions to handle the influx of tracked data and keep them compliant with updated regulations.

Update Your Digital Surveillance System

Another tip when addressing trade surveillance is to think long and hard about your current tech stack — and the type of functionality you might need in the future. Are you using a system that is no longer supported or being enhanced by the provider?

Better analytics tracking systems allow for higher quality alerts and a more transparent, overarching picture of your firm’s surveillance efforts. According to Allied Market Research, the market size of the global trade surveillance system was valued at $780.26 million in 2020, with a projected value of $2.25 billion by 2028. This increase speaks to the high level of trust many financial institutions place in automated, artificially intelligent (AI) monitoring systems. Proactive programs are on the rise and allow organizations to better predict future risk and problematic trader behavior. Similarly, relatively new natural-language processors that intelligently analyze voice and text data for anomalies. Better data collection combined with improved analytics opens up new avenues for firms to enhance their trade surveillance efforts.

An additional advantage of more sophisticated trade surveillance systems is minimizing the number of false-positive alerts. For example, older software processed 10,000 alerts per day and often failed to identify even one confirmed case of abuse. More accurate analytics combined with machine-learning algorithms offer better comparison techniques for weeding out bad behavior and ignoring the more run-of-the-mill trader activities. Metadata analysis allows better visibility into potentially problematic patterns and may help determine intent when dealing with fraud allegations.

Finally, the best trade surveillance tech stacks will include software that provides some form of holistic data aggregation. A review of non-trade items such as accounts, employee records, positions, data changes, licenses & appointments and sales notes, together with trade activity provides a much more complete picture of enterprise risk and a fuller context for evaluating individual transactions. Since RIAs and wealth management advisors interact with their clients in various ways, platforms need to combine voice, written, and automated data into one view that allows firms to take in trade information at a glance.

This move toward “Big Data” requires surveillance technology to accept various formats while delivering a consistent, reliable output to the end user. Ideally, your future trade surveillance system will handle unstructured, ordered, and automated data in a secure, effective way that makes compliance and fraud detection easier and less time-consuming. When it comes down to it, spreadsheets are just not going to cut it in a twenty-first century surveillance environment.

Make Trade Surveillance Central to Your Organization

AI and new tech are great, but internal employee processes must also be adjusted when optimizing trade surveillance systems. Workflow — a combination of digital tools and well-defined manual processes — should be adaptable and allow for as much captured detail on client-trader communication as possible. EY advises firms to develop a strong governance framework that details how to address incidents of fraud and determine culpability. This internal hierarchy could include the order of operations for when alerts are identified, ensuring that the right people take action on the most critical alerts first.

Crafting an employee culture around risk management and ethical practices can also be a critical differentiator for firms practicing successful trade surveillance. Ensuring that risk evaluators follow established processes when critical alerts are identified and complete thorough, accurate investigations — as opposed to quickly opening and closing cases just to “check off the compliance box” — is important to any organization serious about upgrading their surveillance efforts. Ultimately, digital solutions for trade surveillance lose their impact when company culture still enables fraud to occur. Adopting intelligent tech stacks and internal best practices when dealing with potential fraud cases will better ensure that your firm practices effective and compliant trade surveillance.

Financial services and trading involve many moving parts that must be perfectly aligned to succeed. As trading volumes grow and become increasingly complex, the need to monitor every transaction has never been greater or more difficult. Not only do wealth management firms and advisors have to stay on top of data to provide excellent service and results for their clients, but they also have to ensure they stay in compliance.

Automated trade surveillance adds an extra set of eyes to alert advisors to necessary action items and highlight any areas of concern and suspicious activity before they grow into larger — and potentially more costly — compliance issues. Risk management is a moving target, which means time is of the essence and an integrated surveillance system is essential.

Trade surveillance is vital to protecting firms and their clients from unethical trading and fraud. An integrated trade surveillance system monitors a wide variety of data and conditions that can lead to hundreds of alerts a day but focuses on these seven key alerts.

1. Trades

Trading is heavily regulated, but it can be difficult to find patterns in unethical or suspicious trading activity without an automated data program. Trade surveillance tracks when trades occur and keeps an organized audit trail to help advisors stay on top of the process. Alerts can also flag any complications, abnormalities or suspicious trading patterns.

2. Licenses and Appointments

Brokers and financial professionals are required to have the necessary licenses and carrier appointments. Tracking these items and prompting timely renewals allows for trading and compensation processes to proceed smoothly. Financial institutions must proactively ensure their producers are properly licensed and contracted to avoid compliance issues and Not in Good Order (NIGO) exceptions.

3. Data Changes

A key aspect of compliance is ensuring customer data is updated and remains in line with regulations and trading needs. An integrated trade surveillance system can alert you if data has been changed, such as the amount or rate of the trade, or if data needs to be updated to be consistent across all accounts.

Data changes can also relate to suitability and track if the account or trades meet the client’s risk tolerance and investment goals, especially as their data or life stages change.

4. Addresses

Advisors will be alerted if there is an address issue with a trade, including if the address is missing, incomplete, or not consistent across all forms. Scanning addresses to identify address matches to advisor locations or home addresses, or the frequent reuse of an address allow financial firms to spot potential fraud and abuse from insiders.

5. Orders

A comprehensive trade surveillance system pays close attention to an advisor’s order book to ensure every order is in compliance. It keeps complicated orders organized and ensures buyers and sellers meet regulations and have matching criteria.

6. Accounts

Account activity is monitored to identify account exceptions such as large account balance changes, high and low activity accounts, excessive turnover rates and cost to equity exceptions. These alerts can be beneficial for advisors to check in with clients and ensure everything is as it should be and that no fraud has occurred.

7. Sales

A trade surveillance system will likely flag an account with excessive sales or more activity than normal. Advisors can also get alerts if the sales happen before big news or market changes are announced, which could indicate insider trading. Information in the comprehensive contact, account and transaction data base can also be used to improve customer service by notifying producers of life events (e.g. birthdays, anniversaries), monitoring excessive amounts of cash relative to investment objectives, and understanding household structures.

Trading can be a lucrative opportunity for advisors, firms, and clients, but it often comes with high risk and heavy regulations. An automated trade surveillance system is the best way to stay on top of compliance issues while providing excellent service and competitive trades. Less time manually sorting through data and potential issues means more time making deals and growing your business.

Financial firms understand the importance of having a robust and reliable risk management system. Regardless of the size of your clientele, any business that deals with trading, securities and investments has to be aware of the regulatory risks involved. As a result, risk management has become a hot topic both on the industry and federal government level.

For firms looking to enhance (or build from scratch) their risk management efforts, there are three key requirements to keep in mind. Having platforms, people, and processes that identify, remediate, and document risk is essential to the success of wealth management firms in 2022. Without these core characteristics, it’s likely your risk management solution will not stand the test of time.

Consistent and Accurate Identification of Risk

The first key requirement all risk management systems need to have is the ability to consistently and accurately identify risk. An automated data aggregation tool that allows for the scoring and flagging of potential risks is an ideal – and increasingly necessary – investment for firms to seriously consider.

The first piece to this identification process is leaning into a platform that can pull from disparate data sources and visualize findings into a single-view dashboard. Seeing patterns, or otherwise consistent, problematic behavior within trade activity, allows for better threat identification and less wasted time spent chasing false alarms. PWC reported a savings of 160,000 hours through automation of its central services functions in 2019. This achievement not only decreased the manual time employees needed to spend on identifying and evaluating risks, but also expedited the entire process to catch problems before they became too difficult to easily resolve.

Earlier this year, Robert McGill, President, Compliance and Compensation Platforms at Docupace, hosted a webinar focused on topics related to risk management. In this presentation, he particularly focused on the plethora of “false positive” alerts that risk management software generates on a daily basis. Recent reports have identified relationship managers spending up to 60% to 70% of their time on non-revenue generating activities. Unsurprisingly, these alerts cause unnecessary distraction and false lead chasing for back office employees.

McGill argued for the adoption of smart programs that offer a customized solution for categorizing alerts and notifying the right people of appropriate risk levels. Docupace particularly excels at this nuanced handling of threat alerts with its 45 different types that firms can adjust as needed. Having this level of flexibility built into the system allows advisors and investors to quickly adapt and focus resources on the items that need attention rather than dealing with thousands of false alarms.

Similarly, new artificial intelligence technology continues to improve what’s possible when it comes to risk management software. Some programs can better predict future risk through analyzing behavioral patterns. Text and voice analysis better captures conversations with clients into a holistic view of the entire trade exchange. More visibility into every interaction that encompasses a financial transaction provides firms with a better way of determining (and later remediating) risks.

Making Remediation a Priority

The second key piece of risk management is remediation. Remediation refers to the actions taken by RMs (risk managers) and wealth management firms after a threat has been identified. This part of the risk management process typically includes an in-depth follow-up into the risk by a firm representative, extensive documentation, and backfill of available client data.

Perhaps unsurprisingly, many organizations prefer to outsource their remediation operations. In a 2020 survey, over 60% of firms reported a willingness to outsource services that related to operational efficiency. For some companies, investment in an automated technological platform may make the most sense. While still retaining control over sensitive client information and internal processes, software systems like the one Docupace offers better organize and prioritize remediation steps that RMs need to take when dealing with threats. A simplified way of entering notes and tracking complex investigations results in faster and more accurate resolutions, which can save organizations undue time and stress.

Another important component of risk management remediation is developing an extensive governance system to which all employees adhere. EY recently documented its experience developing an ethical employee culture and established processes for dealing with risky behavior. Both front and back-office workers need to view compliance and risk management as a necessity for the smooth operation of business. It’s not good enough to simply “check off the box” when it comes to ensuring safe and transparent trading activity. Instead, employees need to belong to an integrated workflow that has clearly defined roles and practices meant to better manage risk.

Building a Risk Documentation Process

Finally, healthy risk management systems always include a documentation requirement. Federal government regulations and internal procedures often require firms to include documentation of every incident related to risk management. In the pre-digital age, this process very quickly became unwieldy. Mountains of physical paperwork and rows of filing cabinets often defined the work life of financial advisors and risk management specialists. However, new technology has greatly simplified and sped up the risk mediation process regarding trading threats.

Docupace understands the importance of investing in a digital system that organizes and stores documentation. In fact, investing in systems like a DMS (document management system) that store customer data and corresponding documentation can actually be a leading way to attract and retain new talent. Financial advisors excel at client interactions and should avoid work that takes them away from building those relationships and making trades. Solutions like Docupace allow this to happen in a consistent and reliable way.

Ultimately, risk management is a complex subject and one that requires constant organizational adaptation. The more flexible and resilient a firm’s risk management process is, the better it can identify and react to threats that could otherwise result in costs to finance and manpower. Understanding the importance of all three requirements of a risk management system – identification, remediation, and documentation – is not something that companies should take lightly. Building a robust technological solution to this complex and labor-intensive process is what Docupace set out to do – and we strongly encourage all our existing and future clients to continue researching and investing in this key area of business operations.

The annual report from the Financial Industry Regulatory Authority (FINRA), released during the first quarter of the year, lays out new and continuing priorities for financial services oversight in the United States. This year, FINRA CEO Robert Cook noted that much of the new regulations “will be protecting the surge in retail investors who have entered the market in recent years.” Here are the three main takeaways from the report as they relate to broker-dealers and registered investment advisors (RIAs).

Takeaway #1 – The Reg BI Grace Period Is Over

Regulation Best Interest (Reg BI), the SEC’s standard of conduct for broker-dealers, went into full effect on June 30, 2020. And because 2021 was the first full year of implementation, the 2022 report includes several updates to effective implementation. The primary areas of increased focus include “establishing and enforcing adequate written supervisory procedures (WSPs); filing, delivering and tracking accurate Forms CRS; making recommendations that adhere with Reg BI’s Care Obligation; identifying and mitigating conflicts of interest, and providing effective training to staff.” And, as Cook noted during a Q&A with industry executives, that includes re-evaluating processes that were established before the implementation of Reg BI.

Additionally, because Reg BI is now almost two years into implementation, FINRA and the SEC will no longer consider “good-faith efforts” sufficient for compliance. The grace period is officially over — both broker-dealers and registered investment advisors can expect stricter oversight in 2022, and beyond.

Takeaway #2 – Digital Investing is Exploding Online

Although Securities and Exchange Commission (SEC) Chairman Gary Gensler recently announced several initiatives to expand investor protections in the crypto market; indicating that the agency plans to register and regulate crypto exchanges, and will explore separating out asset custody, FINRA is paying closer attention to digital assets and how broker-dealers promote them to investors. Though a more detailed regulatory notice is still forthcoming, firms have been encouraged to keep close tabs on any digital asset-related transactions, including anything that uses a form of distributed ledger technology or blockchain technology. Firms should take extra care to ensure their risk management and compliance systems are up-to-date and prepared to track digital assets.

The report goes on to highlight another tech-driven trend: mobile investing. Apps used primarily by retail investors must have “established and implemented a comprehensive supervisory system for communications through mobile apps.” Additionally, FINRA notes that mobile and web platforms for retail investors must adhere to Reg BI standards in their interfaces and designs, so as not to subconsciously promote certain choices over others.

Finally, FINRA is also applying increased scrutiny on how member firms partner with social media influencers to gain new customers, with Cook highlighting the need for stricter compliance with rules regarding supervision and advertising during a January discussion. The agency is clearly signaling broader oversight of all digital transactions and communications in the future, as finance increasingly moves online.

Takeaway #3 – Evaluations Tighten for High-Risk Firms

FINRA is rolling out its new high-risk regime in 2022, which includes evaluations of any broker-dealers with a significant history of misconduct, or of firms that have a large population of such individuals working for them. Evaluations will start on June 1, 2022 and are expected to continue annually on or around that date going forward (though there will be a bit of a lag between the evaluation date and the formal designation of restricted broker-dealer firms, to account for disclosure reporting delays).

And firms can expect more updates in the future. “We’re probably going to be making some amendments to that regime as necessary going forward,” Cook said. A list of expelled firms, as well as other resources and calculations, will be available in June 2022.